Is it finally time to bottom-fish this stock? Or is it a falling knife?

By Wolf Richter for WOLF STREET.

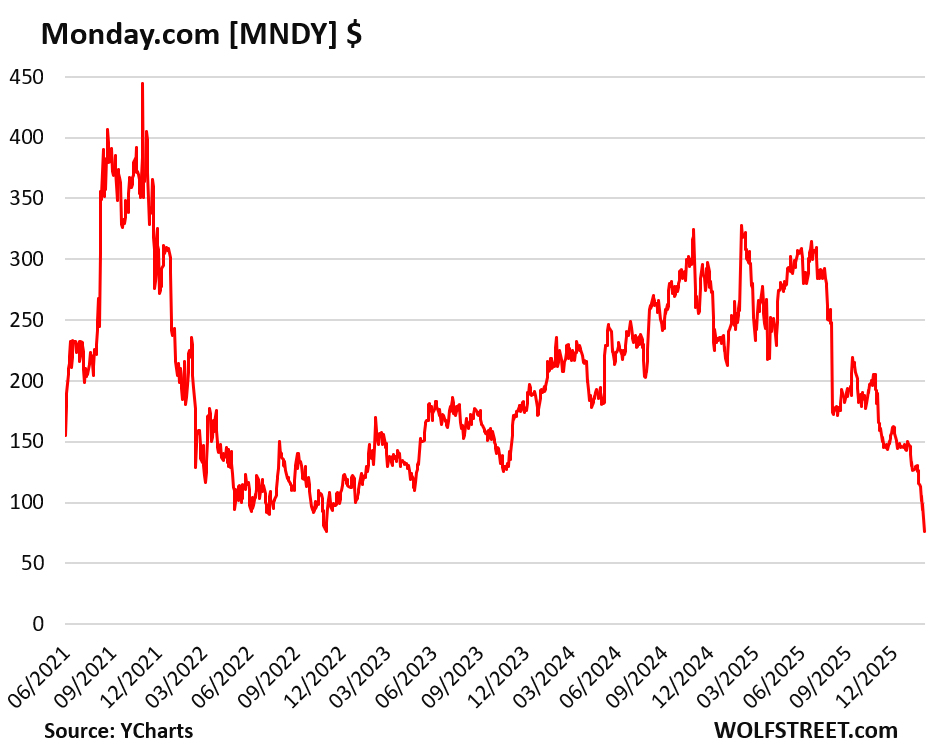

Amid the general repricing of providers of enterprise Software as a Service (SaaS) in recent months, cloud-based collaborative work-management platform with “Agentic AI products,” monday.com, reported earnings this morning, upon which its shares [MNDY] plunged by 22%, to about $76.70 at the moment. If it closes at this price, it will be a record-low closing price.

Since the all-time high in November 2021 ($444.70), the stock has now plunged by 82%, and thereby has become eligible for our pantheon of Imploded Stocks, for which the minimum requirement is a plunge of 70% from the more or less recent all-time high.

The company went public in June 2021 at an IPO price of $155 a share, amid the immense consensual hallucination at the time. Shares are now down by 51% from the IPO price.

In early November, when the stock traded at over $200, 80% of the 25 brokerage firms that cover the stock had a “strong buy” rating on the stock, 8.3% a “buy” rating, and 12.5% a “hold” rating, according to Zacks.

But none had the only rating that would have nailed it: “Sell.” Then, armed with these ratings, the stock plunged by 63% in three months. Why is anyone still paying attention to these ratings?

The stock is traded on the Nasdaq, the company is headquartered in Israel, and files its earnings reports (6-Ks) with the SEC as a “foreign issuer.”

Its Q4 revenues of $334 million, revenue growth of 25%, and adjusted profit of $1.04 per share beat the average of analysts’ expectations.

But its Q1 revenue guidance of $338-340 million fell short; its Q1 revenue growth guidance of 20% fell short; its Q1 guidance for operating income fell short; and its guidance for the full year metrics fell short.

GAAP operating income dropped to $2.4 million in Q4, from $9.6 million a year ago; GAAP operating margin dropped to 1%, from 4% a year ago.

Finally time to bottom-fish this stock? Or is it a falling knife?

I don’t have answers here, only some observations: With GAAP earnings per share in 2025 of $2.24, and even at the current collapsed share price, the stock still has a trailing 12-month P/E ratio of 34.

That’s high for a company that is dialing down its revenue growth rate to 20%, and maybe dialing-down more later amid a whirlwind of software industry challenges, including from AI, perceived or real. The company also continues to issue new shares and thereby continues to dilute existing shareholders: In 2025, its share count increased by 3.1% year-over-year.

At the current price, the stock has a market cap of about $4 billion. The company does sit on $1.62 billion in cash and marketable securities, and it still has revenue growth, though at a slower rate, and those revenues grew to $1.2 billion in the year 2025. And short interest amounts to about 10% of its float, which could make for some fireworks when these folks cover their short positions.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

WOLF STREET FEATURE: Daily Market Insights by Chris Vermeulen, Chief Investment Officer, TheTechnicalTraders.com.

First Appeared on

Source link

Leave feedback about this