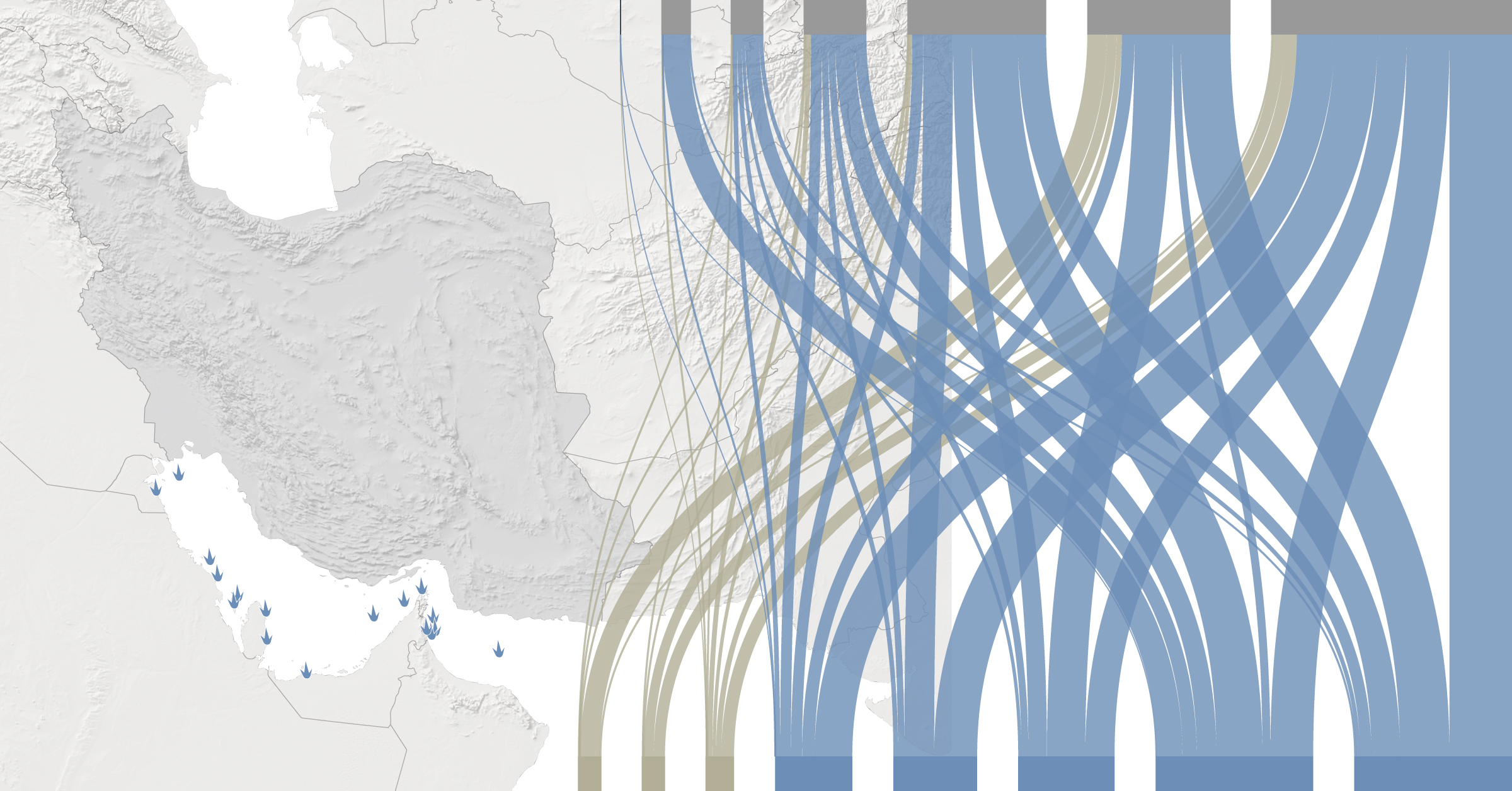

The U.S.-Israeli war on Iran has effectively shut the Strait of Hormuz, the narrow shipping lane between Iran and Oman through which around a fifth of the world’s daily oil and liquefied natural gas (LNG) supply passes. Top Middle East oil producers Saudi Arabia, Iraq, and Kuwait have all cut production at their oilfields because they have to pump oil into storage if they cannot load it onto oil tankers — and their oil storage facilities are brimming after 10 days with no shipping.

The halt to oil and gas shipments through the strait is the nightmare scenario for the global energy system and represents one of the most serious disruptions to energy supply ever suffered. Spare capacity elsewhere in the world is insufficient to plug the gap in supply from the Middle East. Until shipping restarts, refineries worldwide do not have enough crude and will need to run down their inventories to keep producing and supplying fuel to transport and industry. The International Energy Agency is planning to recommend the release of 400 million barrels of oil, the largest such move in IEA history, to help absorb the shock.

Oil prices rose to $119 a barrel on Monday, their highest level since 2022 because of the disruption, though they dropped again before the market closed. If supply disruptions are prolonged, prices could rise further until the recessionary effect of higher energy costs destroys demand. Crude oil, gasoline, diesel, jet fuel, natural gas, petrochemicals, power, and fertilizer prices have all risen sharply since the conflict began.

For consumers and business worldwide, energy costs are rising fast, fueling inflation. Prices for basic foodstuffs have risen as well. Farmers in the Northern hemisphere currently planting their crops are facing higher costs for their inputs.

Asia is the most vulnerable region to supply disruption, relying more heavily on crude, gas and fuel imports from the Middle East than other parts of the globe. Governments across the region are scrambling to deal with the disruption: China has asked refiners to halt fuel exports, South Korea has announced price caps on fuel for the first time in 30 years, and Bangladesh has shut universities to conserve power and fuel.

Only the Strait of Malacca between Malaysia and Indonesia sees more oil tanker traffic than Hormuz. There are few alternatives for the top oil producers that depend on shipping through Hormuz, though Saudi Arabia and the United Arab Emirates are able to send some oil through pipelines that bypass those waters.

Saudi Arabia is pumping crude through its East-West Pipeline from its fields to the Red Sea port of Yanbu. The kingdom typically exports around 6 million barrels per day (bpd) through Hormuz. The pipeline can take up to 5 million bpd, but Yanbu has rarely loaded more than 2.5 million bpd.

The United Arab Emirates also has a pipeline that can transport some crude to bypass the strait. The Abu Dhabi Crude Oil Pipeline (ADCOP), known as the Habshan-Fujairah Pipeline, has a capacity of 1.5 million bpd and transports oil from Abu Dhabi’s fields to the port of Fujairah on the Gulf of Oman.

As well as affecting crude supplies, disruption through the strait is cutting fuel supplies. Refineries in the Gulf have been unable to ship the fuel they produce. That includes Kuwait’s giant 615,000-bpd Al Zour refinery, a key supplier of jet fuel to Europe and Africa.

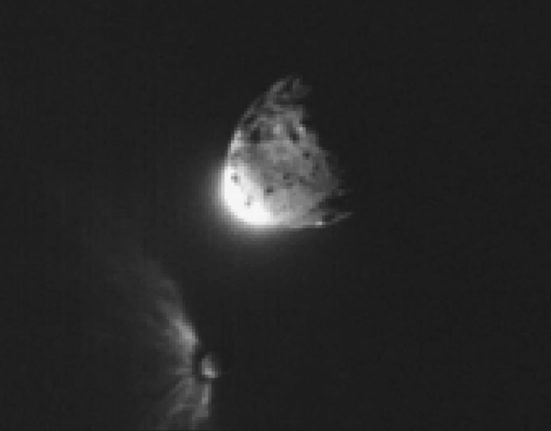

Some refineries have been damaged. Bahrain’s Bapco Energies Sitra refinery, a 380,000-bpd plant, was hit on Monday and declared force majeure. Saudi Aramco shut its largest refinery at Ras Tanura, also the location of the country’s largest marine export terminal, after a drone strike last week.

Even if the conflict ends quickly, repairs will take time to return refineries to normal operations.

Restarting other energy infrastructure will also take time. Qatar’s LNG plant may take several weeks to ramp up from a total shutdown. Oilfields that have reduced production can also take time to recover — and sometimes loss of pressure can lead to a long-term reduction in output.

Shipping costs are also likely to remain elevated due to the risk of drone or other attacks while sailing through the Strait.

For now, hundreds of ships remain anchored on both sides of the waterway as oil and shipping companies watch for any sign that sailings might pick up through the narrow corridor. Tankers around the Strait of Hormuz have come under attack since the conflict began.

Daily volumes of oil and LNG through shipping chokepoints exclude intra-country volumes; The Danish Straits do not include flows through the Kiel Canal; data for the Panama Canal is by fiscal year (Oct. 1—Sept. 30).

Volumes of LNG passing through the Panama Canal are minimal and the EIA does not publish annual data on it.

Daily Brent crude oil price, daily Dutch natural gas price, and daily Asia LNG price data as of March 10, 2026. Weekly percent change in U.S. retail fuel prices and crude oil prices data as of March 9, 2026.

Daily volumes of crude oil and petroleum liquids and LNG come from U.S. Energy Information Administration analysis based on Vortexa tanker tracking and Panama Canal Authority data.

Crude oil and LNG price data come from LSEG Datastream and LSEG Workspace. Retail fuel prices come from the Federal Reserve Bank of St. Louis.

Share of crude and LNG imports to Asia by Middle Eastern countries in 2025 comes from Kpler.

Volume of origin and destination supplies of crude and liquefied natural gas data over the last 14 months comes from the LSEG Shipping platform.

Imagery of oil infrastructure and tanker damage provided by Vantor, REUTERS/Amr Alfiky and Reuters.

Locations of damage to infrastructure and tankers are from Reuters reporting.

Additional design and development by

Tiana McGee, Mayank Munjal

Emily Chow, Sudarshan Varadhan

Ella Koeze, Simon Webb, David Gaffen

First Appeared on

Source link

Leave feedback about this