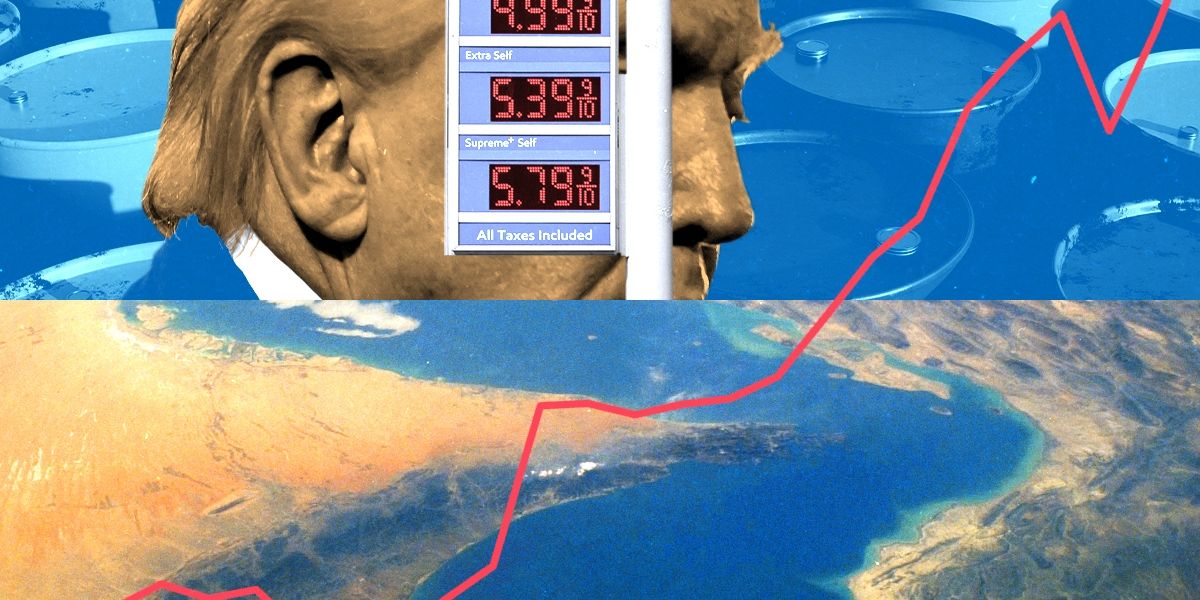

No matter how much longer the United States and Israel’s war with Iran lasts, the world’s energy system will be grappling with its consequences at least through the end of the year, if not for far longer.

The biggest short-run effects of the Iran energy crisis will be felt in Asia, where economies that run on Persian Gulf oil and gas face shortages and higher prices. The supply shock has — and will — drive up prices, leading oil and gas producers who aren’t stuck behind the Strait of Hormuz to seek higher returns. Much of the continent is already in the midst of an energy crisis, complete with fuel rationing and top-down policies to reduce oil and gas consumption.

In Australia, gas stations are running out of diesel. The government of the Philippines adopted a four-day workweek to reduce commuting. Pakistan announced a two-week school closure. Nepal is rationing cooking fuel. Thailand’s prime minister told civil servants to take the stairs, and the government set air conditioning to a minimum 79 degrees Fahrenheit.

Around the world, coal use is rising. Gasoline prices are on the way up, even in the United States, which is a net exporter of crude oil and petroleum products. Even if the war were to end tomorrow, oil and gas markets are likely to remain tight for many months to come.

Just as the oil shocks of the 1970s transformed the economies of the then-rich world — spurring the takeoff of nuclear power to in Japan and France; pushing the U.S. to direct R&D funding and subsidies to solar and shale gas; motivating carmakers around the world to developer smaller, more fuel-efficient vehicles — so too will this crisis likely transform how the entire world structures its dependence on oil and gas. It maybe already has.

Let’s take an industry-by-industry look:

Oil

The year began with a global oil glut. That has long since vanished. No matter what happens in Iran over the near to medium term, expect the oil market to remain tight.

Before hostilities with Iran ramped up, the consensus was that the market was “oversupplied,” Greg Brew, an analyst at the Eurasia Group, told me. “Demand growth was expected to be fairly sluggish. Production from OPEC states and the U.S. was expected to be fairly high, and prices were going to be in the $60s and potentially $50s [per barrel]. Obviously that is now completely out the door.”

Both Goldman Sachs and Morgan Stanley analysts speculated that the Brent crude benchmark could hit or even exceed its 2022 high of around $122 a barrel. It might even break through its all-time high of around $150, reached in 2008, should the closure persist.

Even if the strait were to reopen tomorrow, it would leave a large “air pocket” in the oil market, Morgan Stanley oil analyst Martijn Rats wrote in a note to clients last week, referring to oil that will never come to market because of shut-in production. That would keep prices high through the second and third quarters of the year as supply catches up to demand.

Oil analyst and author of the Commodity Context newsletter Rory Johnston estimated that the size of this “air pocket” is in the hundreds of millions of barrels. “Inventory will start dropping like a rock” over the coming weeks, he told me, “even if we could snap fingers and just go back to where we were two, three weeks ago.”

That squares with what Brew told me, as well. “Even when Hormuz reopens, the price band through the rest of the year is unlikely to fall below $75 a barrel, given the size of the physical disruption that we’re experiencing,” he said. A barrel of oil cost around $60 at the end of last year, before the price began to creep up as the U.S. gathered forces around Iran.

There will likely still be a “sustained risk premium” for any tanker leaving the strait as long as the current Iranian regime remains in power, Brew said. “The most likely outcome from this war is one where Iran is weakened but has not collapsed — where it retains the capabilities to threaten traffic through the strait and to threaten [Gulf Cooperation Council] states.”

Natural gas

A supply squeeze that could have resolved quickly once the Strait of Hormuz reopened and Qatar’s Ras Laffan facility got up and running again turned into a years-long interruption when Iran knocked out 17% of Qatar’s liquified natural gas export capacity, taking out almost 13 million tons per year of gas production, according to Morgan Stanley. As recently as a month ago, Qatar supplied about a fifth of global LNG capacity. The damage will likely take several years to fix, the chief executive of QatarEnergy told Reuters.

“What started as a transitory (but significant) capacity outage has escalated to a multi-year loss of supply,” Morgan Stanley analysts wrote in a note to clients Thursday. “Even with near-term resolution, the global gas market will need to contend with refilling inventories amid a large supply loss, creating upside price risks.”

European and East Asian LNG importers will likely choose to pay the higher prices. Poorer countries in South and Southeast Asia, however, may have to go without.

“There is now no longer going to be an LNG glut in 2026. There’s going to be a tight gas market,” Brew told me. “That’s going to keep regional prices high. That’s going to keep European prices high. That’s going to keep Asian prices high. That’s going to mean emerging markets in South Asia and Southeast Asia that would otherwise be able to buy LNG cargoes are going to have a tougher time.”

Much of the rationing of electricity or the shutdown of fertilizer plants in South and Southeast Asia was already happening before this week’s catastrophic attacks, the result of Qatar cutting off production due to earlier strikes.

No matter how long the war lasts, European and Asian gas buyers will have to refill their gas reserves before winter sets in again, which will further strain an already tight market. The Morgan Stanley analysts said prices are more likely to go up than down through the rest of the year even if there’s deescalation soon.

Jefferies analyst Julien Dumoulin-Smith wrote in a note to clients Wednesday that “even if the disruption proves temporary, LNG’s perceived risk profile has likely shifted structurally.”

“The conflict has underscored how concentrated global LNG supply remains around a narrow choke-point. That realization alone may embed a higher risk premium in LNG pricing,” he wrote. “Over time, higher prices could slow demand growth among some price-sensitive buyers and alter how buyers assess long-term LNG investment decisions.”

Coal

Just like in 2022, countries that suddenly find themselves short on natural gas will almost certainly turn to coal. “My sense is that this is going to be great for coal as 2022 was,” Brew said, referring to the uptick in coal usage following the Russian invasion of Ukraine, which cut off a major source of natural gas supply for Europe.

In both Europe and Asia, the “coal equivalent” price of gas has shot up, meaning that natural gas is now much more expensive on a dollars-per-unit-of-energy basis. This will incentivize switching to dual use gas and coal plants, or else bringing under-utilized coal-burning power plants into service, especially in Asia.

South Korea said earlier this week that its nuclear and coal power plants could raise their output in light of reduced LNG availability. South Korea is heavily dependent on both fossil fuels and imported energy — 84% of its energy supply is imported on net; almost 80% of its energy supplies are fossil fuels, and about 15% of its LNG imports come from Qatar.

The energy consulting firm Wood Mackenzie estimated that coal-fired power plants in Japan and South Korea could offset 70% and more than 100% of their gas-fired generation, respectively. But, Wood Mackeznie noted, that’s only in the current “shoulder season,” when mild weather means less electricity demand. “If disruptions persist into peak summer demand, the effectiveness of coal as a buffer will diminish, increasing exposure to tighter supply conditions.”

In Europe, which invested heavily in renewables and gas imports (largely from Norway and the United States) following the Russian invasion of Ukraine, coal’s cost favorability to natural gas is improving, but overall demand has been falling as days get longer and warmer. In Germany, coal’s share of electricity generation rose 2% in March compared to February.

Solar, wind, and other forms of clean energy

There are already anecdotal reports of enthusiasm for renewables picking up in light of the fossil fuel supply shock. Bloomberg reported that electric vehicle showrooms are filing up across Asia with interested buyers looking to avoid expensive and sometimes rationed fuel.

Oil demand, particularly in Asia, “will be lower than it was before the war in terms of the expectation,” Johnston said. “There is no possibility, in my mind, that we do not see an enhanced drive toward energy efficiency, electrification, and other forms of diversification. It’s just the obvious outcome of this.” He said the amount of vulnerability Asia has to oil and natural gas is “existential” and “not tolerable.”

“Energy security and affordability is a much more compelling political argument” for a transition to clean energy than moral arguments about preventing future climate change, he added.

The same could be true for natural gas, especially LNG. The “next leg” for LNG growth globally, Dumoulin-Smith wrote, was supposed to be “price-sensitive demand in South/Southeast Asia.” That growth could be put at risk by “sustained higher prices” that induce “demand destruction, fuel switching (notably coal), delayed downstream infrastructure investment, or possibly ‘skipping’ LNG as a transition fuel in favor of renewables.”

In a note sent to clients Friday, Dumoulin-Smith wrote, “We see a constructive demand tailwind for U.S. clean energy peers beyond 2026,” due to “the multi‑year energy challenges implied by the escalation” of attacks on energy infrastructure in the Persian Gulf.

Even in the United States, which is more insulated from some of the worst shocks (we’re not going to run out of natural gas anytime soon), now may be a good time to “be stepping back and thinking a little bit more holistically about how we’re structuring our energy policy and our energy systems,” Francis O’Sullivan, managing director at S2G Investments, told me.

“We need to take a more all-of-the-above type approach to our energy system and our energy policymaking than is currently the case.”

There are ever-so-slight signs of a thaw toward renewables and in favor of an all-of-the-above strategy in the U.S. The federal government late last week declined to appeal a federal court ruling in favor of offshore wind developers who sued the Department of the Interior over its stop work orders. Senate Democrats have said they’re once again open to a deal with Congressional Republicans and the White House to ease permitting for all types of energy projects.

First Appeared on

Source link

Leave feedback about this