Live Updates

Live

Here’s the key highlights from Oracle’s conference call:

First 20/20 Quarter in 15 Years

CFO Doug Kehring set the tone early: “Q3 being the first quarter in over 15 years where both organic total revenue and organic non-GAAP EPS grew at 20% or better.” A milestone that immediately signaled this was no ordinary earnings call.

TikTok Stake Now Official

Oracle quietly became a stakeholder in one of the most talked-about companies on the planet. Kehring confirmed Oracle now holds a 15% equity stake in TikTok US following its separation from ByteDance, with a seat on the board. The financial impact hits Q4 results.

$30 Billion Raised in Days

The capital markets loved what they saw. Oracle announced a $50 billion financing program and almost immediately raised $30 billion through bonds and preferred stock. Kehring noted the order book was “substantially oversubscribed” — a sign Wall Street is firmly behind Oracle’s expansion.

Cloud Software Business Firing on All Cylinders

Co-CEO Mike Sicilia was direct: “Oracle has the fastest growing, most complete suite of cloud applications in the market, full stop.” Cloud applications hit a $16.1 billion annualized run rate, up 11% in constant currency. Fusion ERP up 14%, HCM up 15%, SCM up 15%, NetSuite up 11%, industry software up 19%.

The “SaaS Apocalypse” Rebuttal

Sicilia addressed the theory head-on that AI startups will kill traditional software companies: “Some smaller or single focused SaaS players may well be disrupted, but Oracle will not be among them.” His reasoning — Oracle covers entire business ecosystems end to end, something no startup can replicate quickly.

1,000+ AI Agents Already Embedded

While competitors are still talking about AI, Oracle is already delivering it. Sicilia confirmed Oracle has “delivered well over 1,000 agents right inside our horizontal back office and industry applications” — built into existing products at no extra charge to customers.

Three New AI Sales Tools Salesforce Doesn’t Have

Oracle launched three brand new AI-powered sales applications — lead generation and qualification, sales orchestration, and automated selling. Sicilia’s pointed jab: “These are 3 products that Salesforce.com does not have.”

531% Database Growth. Not a Typo.

Co-CEO Clay Magouyrk dropped the biggest number of the night: “Multi-cloud database revenue grew 531% year-over-year.” He added that AI infrastructure revenue grew 243% year over year. The problem, he said, isn’t demand — it’s keeping up with it.

Now Inside Every Major Cloud

Oracle’s database used to live only on Oracle’s own cloud. That’s changed dramatically. Oracle is now live in 33 Microsoft regions, 14 Google regions, and expanded from 2 to 8 Amazon regions during Q3 alone. Target: 22 AWS regions by Q3.

Live

Updates will slow down as we’re listening to Oracle’s conference call. If you leave this page open, we will release an earnings call summary after it concludes. Simply refresh this page later if you’re looking for analysis on what Oracle says on its call.

Live

Shares are up 8%, watch the key points we highlighted earlier; they will determine whether shares gain more or fade into the open tomorrow.

Live

Oracle’s shares are holding to 8% gains. The next big test will be the company’s conference call, which begins at 5 p.m. ET.

Expect Wall Street to ask about the following:

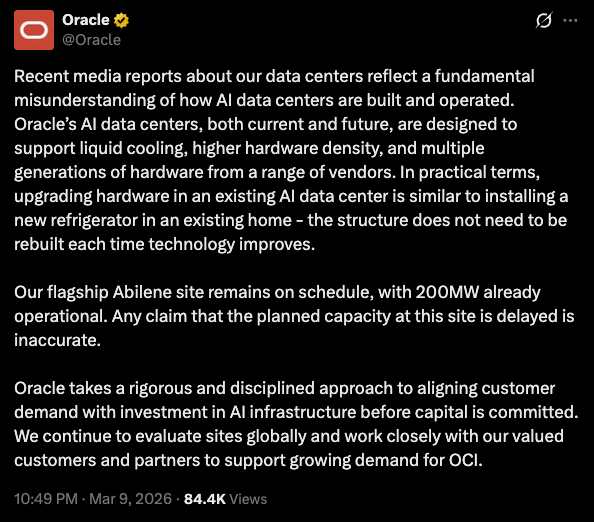

- Recent Reports About Abilene Stargate: Bloomberg published a story on Abilene on Friday afternoon. Expect management to address this report and how it fits into their future strategy.

- Customer Concentration: Wall Street will continue poking at how much of Oracle’s RPO is OpenAI. The most Oracle can speak to customer diversification, the more a key risk is removed from the site.

- CapEx Questions: Oracle didn’t make any revisions to its capex plans in its earnings release, but we’d expect Wall Street to try asking some clever questions to infer whether Oracle’s spending plans have adjusted in the past quarter.

Live

With the headline numbers and guidance already digested, four surprises stand out as likely drivers of tonight’s after-hours move.

The biggest is IaaS growth accelerating. Cloud Infrastructure grew 84% YoY to $4.89 billion, up from 68% growth last quarter. Acceleration was not widely expected, and it directly counters the narrative that Oracle’s AI infrastructure buildout was hitting a ceiling.

Second, the RPO surging 325% YoY to $553 billion is a forward-demand signal of unusual magnitude — and critically, many of these contracts involve customer-supplied GPUs, reducing Oracle’s own capital burden.

Third, the FY2027 guidance raised to $90 billion exceeded the $86.4 billion Wall Street consensus.

The negative surprise: restructuring charges more than doubled to $153 million from $63 million a year ago – a cost signal worth monitoring heading into Q4.

Live

Here are some of the biggest growth rates from tonight’s Oracle (ORCL) Q3 earnings:

- Cloud Revenue: Up 44%

- Infrastructure Revenue: Up 84%

- RPO: At $553 billion

- Fiscal 2027 Revenue Guidance: $90 billion (Tops Wall Street guidance of $86 billion)

- EPS Outlook: $1.98 at midpoint (Wall Street expected $1.94)

In short, every metric so far has beaten Wall Street forecasts.

Live

With Oracle’s Q3 results now in hand, it’s worth revisiting which wildcards actually materialized tonight.

The two factors that mattered most: RPO conversion pace and restructuring charges. As flagged ahead of the report, the gap between Oracle’s massive backlog and recognized revenue was the central tension. Q2’s revenue missed estimates despite RPO exploding 438% YoY to $523 billion — tonight’s beat suggests conversion is finally accelerating.

The tariff wildcard remains unresolved. Kalshi prediction markets put only a 23% probability on “tariff” being mentioned on the call — low conviction, but elevated macro trade tensions mean it could resurface in Q4 guidance commentary.

GPU supply constraints bear watching as capex guidance of $50 billion signals Oracle is betting big that chip availability holds.

Oracle’s call starts at 5 p.m. ET.

Live

Oracle stock initially jumped 3% and then took another step up to 8%.

We’ll see if these gains hold as Wall Street digests these earnings. The company raised revenue guidance and importantly also hasn’t provided updates on capital expenditures.

Live

Oracle shares continue to climb as Wall Street digests not only last quarter’s beat, but guidance for $90 billion in revenue next year.

It’s welcome news for investors who have seen shares battered.

Live

Oracle updated its outlook for the year.

- Revenue: $67 billion (largely in line with Wall Street expectations)

- Capital Expenditures: $50 billion

- Fiscal 2027 Guidance: Raised to $90 billion

Wall Street was expecting $86.4 billion in revenue next fiscal year.

Live

Oracle’s (ORCL) earnings are out, here are the most improtant numbers.

- EPS: $1.79 (against expectations of $1.69)

- Revenue of $17.19 billion (beats expectations of $17.19 billion)

Shares have initially spiked 3.3% on the news. We’ll continue digging into earnings.

Live

Oracle earnings are expected to drop at 4:05 p.m. ET.

If you stay on this page live updates will post automatically. We will begin providing news and analysis the moment earnings are released.

Live

We are now just 10 minutes until Oracle’s Q3 earnings. As a reminder, here’s what Wall Street expects:

- EPS: $1.69

- Revenue: $16.9 billion

Looking ahead to Q4, here’s what Wall Street currently has for Q4.

- Adjusted EPS: $1.92

- Revenue: $19.1

The big story continues to be Wall Street’s discomfort with how aligned Oracle is with OpenAI. The broader ‘OpenAI complex’ of stocks (including Oracle, ARM, and NVIDIA) has struggled across the past six months.

OpenAI just raised $100+ billion at a pre-money valuation of $730 billion and will likely IPO this year. Yet, the company is losing market share to Anthropic. Wall Street is neverous their model is unsustainable.

You also see this in how every headline around Oracle becomes ‘sell first, ask questions later.’ Friday’s Bloomberg report sparked fear across markets, and has led to several respons from Oracle including this one today.

Market sentiment is very negative around Oracle right now, we’ll see if tonight can reverse it.

Live

AI infrastructure stocks in general have had a good day, but Oracle (ORCL) shars remain under pressure. As of 3:35 p.m. ET, they’re down about 1%.

We’ll see if tonight’s earnings can be a catalyst that start turning Oracle’s continuing stock slide around.

Oracle reports its fiscal Q3 2026 results after the bell tonight, March 10, 2026. The stock is trading at $151.12, down 22.05% year to date and sitting well off its 52-week high of $344.21. That kind of drawdown heading into an earnings print creates real stakes tonight.

What Wall Street Expects

The consensus EPS estimate for tonight is $1.69. Revenue estimates for the quarter sit at $16.9 billion.

Oracle carries a forward P/E of 19x at current prices, with an average analyst price target of $253.08, implying significant upside from here if the cloud growth story stays intact.

The prediction market on Polymarket puts the probability of an earnings beat at 78%. Oracle has beaten EPS estimates in 4 of the last 8 quarters, so the crowd is leaning more optimistic than history strictly warrants.

Last Quarter Recap

Oracle’s Q2 FY2026 report in December was a study in contradictions. EPS came in at $2.26 against an estimate of $1.63, a massive beat. But shares plunged roughly 12% after management unveiled an aggressive capital spending plan that rattled investors focused on near-term profitability.

The EPS beat was partly inflated by a one-time $2.70 billion Ampere divestiture gain. Underneath that, cloud infrastructure revenue grew 68% year over year, and the remaining performance obligation hit $523 billion, up 438% year over year. The backlog is enormous. The question is how much Wall Street fears continuing concentration to OpenAI.

As CNBC recently noted, Oracle may be the canary in the coal mine for AI infrastructure deals, making tonight’s commentary on deal flow and cloud demand especially important for the broader sector.

What to Watch Tonight

- IaaS revenue growth rate: Last quarter it hit $4.079 billion, up 68% year over year. Analysts want to see that momentum hold or accelerate. A deceleration here would be the single biggest negative signal.

- RPO conversion: A $523 billion backlog only matters if it turns into cash. Management’s commentary on how quickly that converts to revenue will be closely parsed.

- Capex guidance and free cash flow: Oracle spent $20.535 billion on capex in just the first half of FY2026. Investors will carefully study comments around future capital expenditure plans.

- Software license drag: Software license revenue declined 21% year over year last quarter. If that legacy erosion accelerates, it pressures overall growth even as cloud shines.

- Stargate and AI deal commentary: Prediction markets put a 63% probability on the Stargate project being mentioned on tonight’s call. Any update on that contract could move the stock meaningfully.

That last point is important as Bloomberg published a story Friday afternoon on Oracle backing out of future expansions at Stargate Abilene. The company has said they’ll still finish most of the project and instead of prioritizing other projects. We’ll see what specifics the company provides, I’d expect this to be a key them on Oracle’s conference call.

First Appeared on

Source link

Leave feedback about this